[ad_1]

Michael Vi

Investment Thesis

Charter’s (NASDAQ:NASDAQ:CHTR) last quarter was worse than expected. The company reported a decline in internet subscribers. Net subscriber adds in this segment have been critical to the company’s long term revenue growth.

I think there are some promising trends, such as a small jump in ARPU and the strong growth of Spectrum Mobile. But I am still waiting for a clearer growth trajectory before I’d personally buy shares in the company.

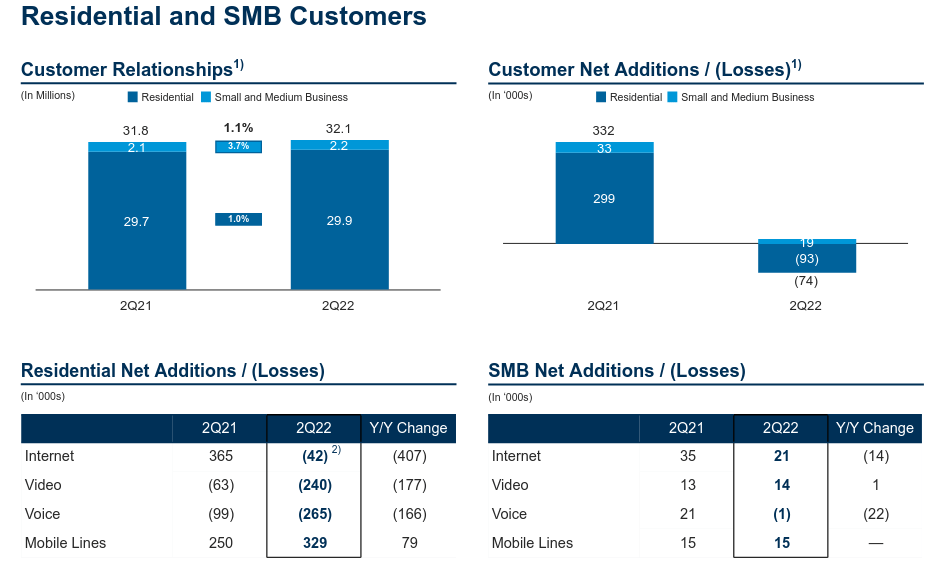

Subscriber Growth Slowdown

The major takeaway from Charter’s second quarter is that growth is declining. The company reported a net loss of 21,000 internet subscribers. Management attributes these losses to the discontinuation of a COVID relief program. But removing this headwind doesn’t change much. The company would still have only gained 38,000 subscribers. This is down from 400 thousand adds in the second quarter of last year. It’s the first time since before the pandemic that the company has gained fewer than 185,000 internet subscribers in a quarter.

Charter Q2 Earnings Presentation

My primary concern with Charter is the company’s growth trajectory. The business’s strategy is largely based around customer growth through lower prices. The company has used its strong internet subscriber growth as the core of its business. This growth has offset secular declines in its legacy video and voice businesses.

Management thinks that we’re in a very low growth environment for internet services. Customer churn is extremely low. This has reduced the opportunities for new subscriber acquisitions. But I find it difficult to reconcile this claim with the strong reports from other companies’ internet offerings.

During their second quarter, T-Mobile (TMUS) alone added 560,000 subscribers to their fixed wireless offerings. That company predicts a similar or higher run rate in the future. It’s clearly possible to make gains in the current market. This should be especially true for a company with low market penetration. Charter’s management regularly mentions their low share of household connectivity spend in their footprint.

I think management may be underestimating their competitors. Fixed wireless and fiber expansion may be a significant headwind. It’s too early to say positively, but it’s a risk that I haven’t seen discussed often.

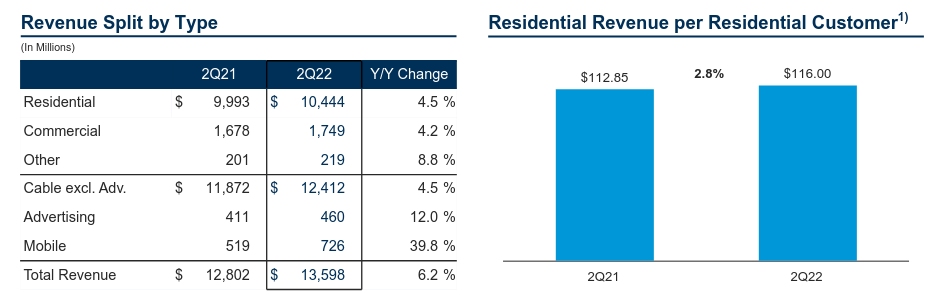

Average User Revenue Update

In spite of user losses, Charter reported decent top line numbers. Revenue was up more than 6% year over year and 3% sequentially. This was driven by an uptick in average revenue per customer.

Charter Q2 Earnings Presentation

Residential ARPU increased from $113 to an all-time high of $116 during the quarter. Management attributed this to promotional rate step ups and video rate adjustments. I’ve been critical of the company’s stagnant ARPU in the past, so this may be a sign of improvement. It’s too early to call this a definitive trend, but I find this promising.

Is Spectrum Mobile A Good Growth Driver?

Charter is also working to add new offerings for its customers. The company’s Spectrum Mobile segment was a bright spot during the last quarter. It was the only consumer segment that posted positive sequential growth. And that growth is accelerating.

Charter’s mobile strategy is interesting. It blends usage of the company’s wireless network with an MVNO on Verizon’s (VZ) network. This partnership lets Charter provide a solid service with its competitive pricing strategy. So far, it has been a success, growing almost 40% year over year. The rate of user adds is increasing as well. The company added 344 thousand mobile lines in Q2, up from 265 thousand last year.

This is a good opportunity to drive incremental revenue from Charter’s existing customers. It may help ease my ARPU concerns and boost growth in a low user acquisition environment. The segment is currently even capable of generating a sustainable profit on its own. On their last earnings call, management discussed their wireless services’ profitability profile.

On the wireless, the — it is increasingly important, and I don’t think it’s well understood by the marketplace. It has a reported EBITDA loss right now, but that’s entirely driven by subscriber acquisition cost for sales and marketing. The EBITDA for wireless passed the positive point really some time ago. I don’t remember what quarter, but it’s probably a year plus. So it’s an attractive product, and we’re growing it fast, and I — we’re not going to get into margin analysis or forecast. But I will tell you that the — everything that I’ve ever looked at that people publish on the topic grossly underestimates our margin that’s inherent inside that business and what we can do with it to drive the business overall, including broadband net additions. So it’s powerful. I don’t think it’s very well understood, and that’s okay for now.

The segment is still in its early stages. It only makes up 5.3% of Charter’s revenue at the current run rate. But this proportion has doubled over the past two years, and its growth rate has been increasing over the past few quarters. I think this segment could be an important growth driver in the future.

Buybacks, Debt, and Valuation

Charter’s capital allocation strategy is heavily focused on share repurchases. The company spends most or all of its operating cash flow buying back its own shares. This has drastically reduced the company’s share count. In the last two quarters alone, the company has bought back almost 7% of its shares outstanding.

Charter Q2 Earnings Presentation

But this strategy does have a cost. Telecommunications businesses are very capital intensive. Charter’s capital expenditures have been funded primarily through debt. This can be a useful strategy in some circumstances. But Charter’s debt burden recently surpassed the company’s market cap. If the company doesn’t sustain strong growth, management will likely have to pivot to paying down debt at some point. This could severely impact shareholder returns.

Charter is trading at an EV/EBITDA of 7.5 times and an EV/OCF of 10 times. I think this valuation is reasonable for a company with slow but steady revenue growth and faster bottom line growth. But I am still concerned about the company’s long term ability to return cash to shareholders.

Final Verdict

There’s a lot to like about Charter’s stock. It’s a growing company that is trading at a cheap valuation. The business generates strong free cash flow and consistently returns cash to shareholders.

But recently, the company’s subscriber growth has started experiencing some headwinds. The business’s high net debt levels are increasing. I still think the company could be undervalued. But I want to see evidence of sustained growth in either internet subscribers or ARPU before I’d confidently buy in.

Source link