[ad_1]

Morsa Images

Company Overview

Upwork Inc. (NASDAQ:NASDAQ:UPWK) has fallen 47% YTD due to macroeconomic issues and slower growth. However, its business fundamentals are sound as it has successfully implemented several strategies for revenue expansion from its existing customer base. Still, my recommendation is a “HOLD” as it’s richly valued and I believe that investors should wait for better buying opportunities.

The Market

Upwork’s market was worth about $4.5 Bn in 2021, giving them roughly 11% of the market share. Freelancing is a fast-growing trend, with McKinsey estimating that 500 million freelancers will be working through platforms before 2030 and estimated to be the U.S majority workforce by 2027. Workers are turning into freelancers because of declining employee engagement and trust in company leadership. This has been worsened by companies’ mandates to return to the office. Businesses have been receptive to the changing workforce, with 70% of SMBs in the U.S having worked with freelancers and 81% planning to hire freelancers again. As a result of these tailwinds, the market is expected to grow to $9.19 Bn by 2027, with an impressive growth CAGR of 15.3%.

Upwork Earnings Analysis

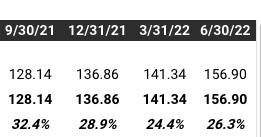

In Q2 2022, Upwork reported $156.9M in revenue, which increased 23% YoY and beat expectations by $9.12M. Its EPS was -$0.04, which beat expectations by $0.04. Despite short-term disruptions in Europe, Upwork is raising its revenue guidance for FY 2022 to be between $612 million and $617 million versus the consensus of $597.04M, representing an average growth of 22% YoY.

Sound Fundamentals

Due to the current macroeconomic conditions, Upwork’s growth has seen a slight decline.

TIKR Terminal

Management further estimates a $10 to $15 million impact from these conditions. However, impacts from the global macro environment are much less for Upwork and might instead provide tailwinds for further growth. If economic conditions worsen, companies will be forced to cut costs-one of which includes switching to freelancers in order to avoid the overhead costs of a traditional workforce. In addition, management reported in their Q2 call that its newly launched client marketplace plan has been doing well for the company. This strategy streamlines the user experience, lowers friction, and also provides all self-service customers greater features for a set service cost. This plan further incentivizes SMBs to stay on the platform amidst their need to cut costs. As a result, the marketplace take rate increased from 13.2% to 14%, and management anticipates that marketplace income and takes rate will continue to rise in upcoming periods. Finally, Upwork has been very successful in acquiring enterprise customers as a result of their stellar sales team (which they plan to double by the end of the year). Upwork has seen its enterprise revenue increase 45% YoY to $12.3 million as well as a significant increase in million-dollar spenders. Upwork’s focus on acquiring large customers will strengthen its ability to generate FCF amidst uncertainties in the macro environment.

Valuation

Because Upwork is currently cash flow negative, I will be calculating Upwork’s valuation based on its revenue and P/S ratio. If we assume that Upwork retains its 11% in market share in 2027, that leaves its revenue at $1.01 Bn. Using a 4x P/S ratio (down from its current 4.18), its market capitalization would be $4.04 Bn in 2027. Discounting it back with an 8% discount rate, leaves its intrinsic market capitalization at $2.75Bn, or a 26% upside from its current price. This method is not the most conservative; thus, I believe 26% is too little of a margin of safety.

Risk

The biggest risk to Upwork’s growth remains to be from Europe. The energy crisis will have grave consequences on its economy and trickle down to strongly impact the ability of SMBs to survive. In addition, Upwork’s valuation is strongly dependent upon its ability to grow fast. The combination of high-interest rates and slower growth as a trend could slash the company’s valuation. Although it’s entirely possible for Upwork to excel and perform much better than what my method suggests, any slight hiccups to its growth will significantly hurt its valuation at its current prices.

Conclusion

Upwork is in a promising market that will surely see strong demand in the coming years. Although growth has slowed, its business fundamentals are in a position to endure the macroeconomic conditions. Still, its valuation presents a small margin of safety, and I personally will be waiting to get in the stock at better buying opportunities or at least until the situation stabilizes in Europe.

Source link