[ad_1]

tawatchaiprakobkit/iStock via Getty Images

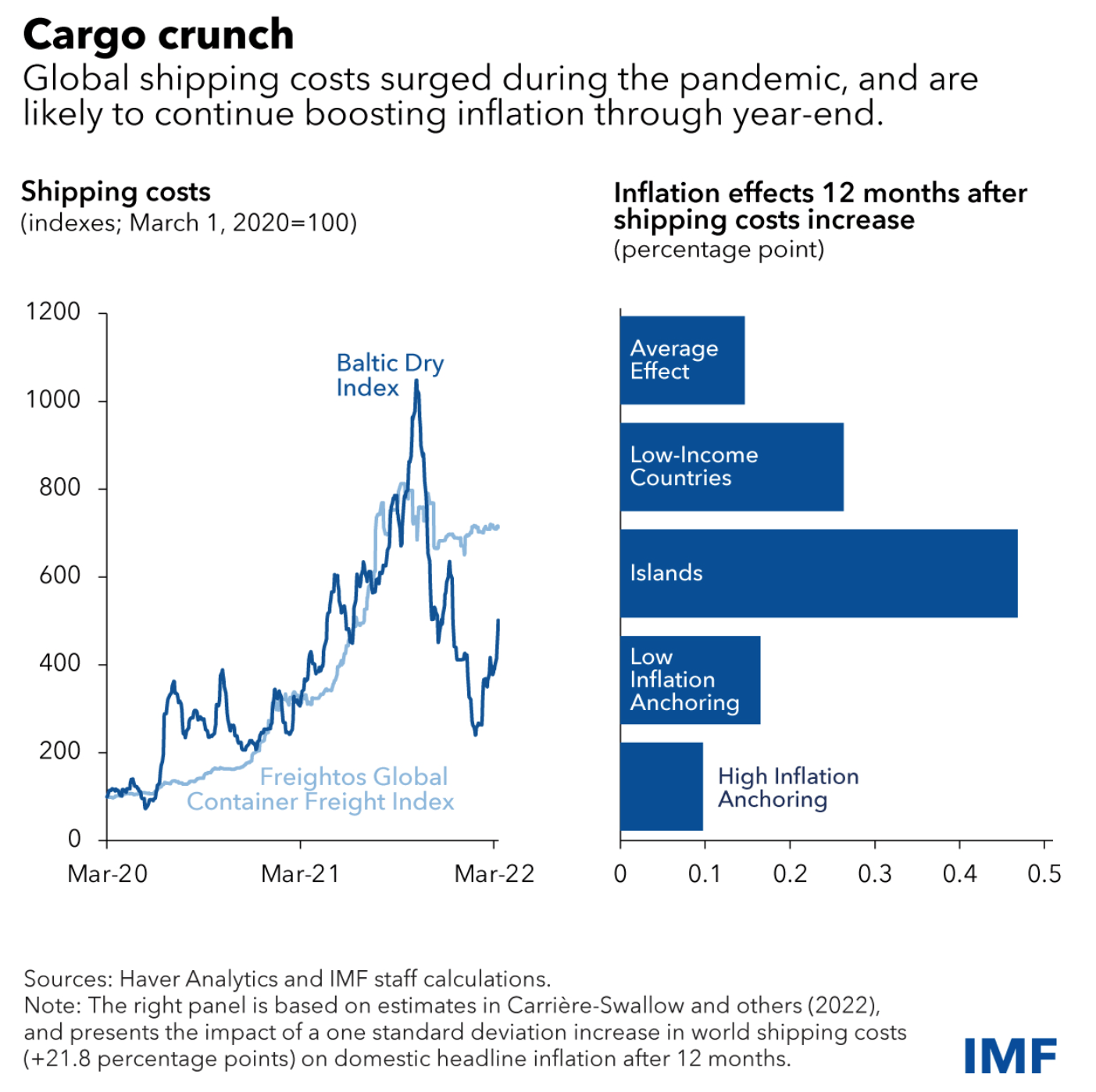

ZIM Integrated Shipping Services (NYSE:ZIM) is a global cargo shipping company, which is one of the top 20 carriers. The company was founded back in 1945 and strategically chose the perfect time to IPO in January 2021. At that point shipping costs exploded, due to the demand shock of the economy reopening, which has been dubbed the “Cargo Crunch”. According to a recent study by the IMF, Global Shipping costs are linked to increasing inflation. The study which spans 30 years’ worth of data from 143 countries, shows some interesting correlation, here is a direct quote from the IMF Report:

We find that shipping costs are an important driver of inflation around the world: when freight rates double, inflation picks up by about 0.7 percentage point. – IMF (March 28th 2022.)

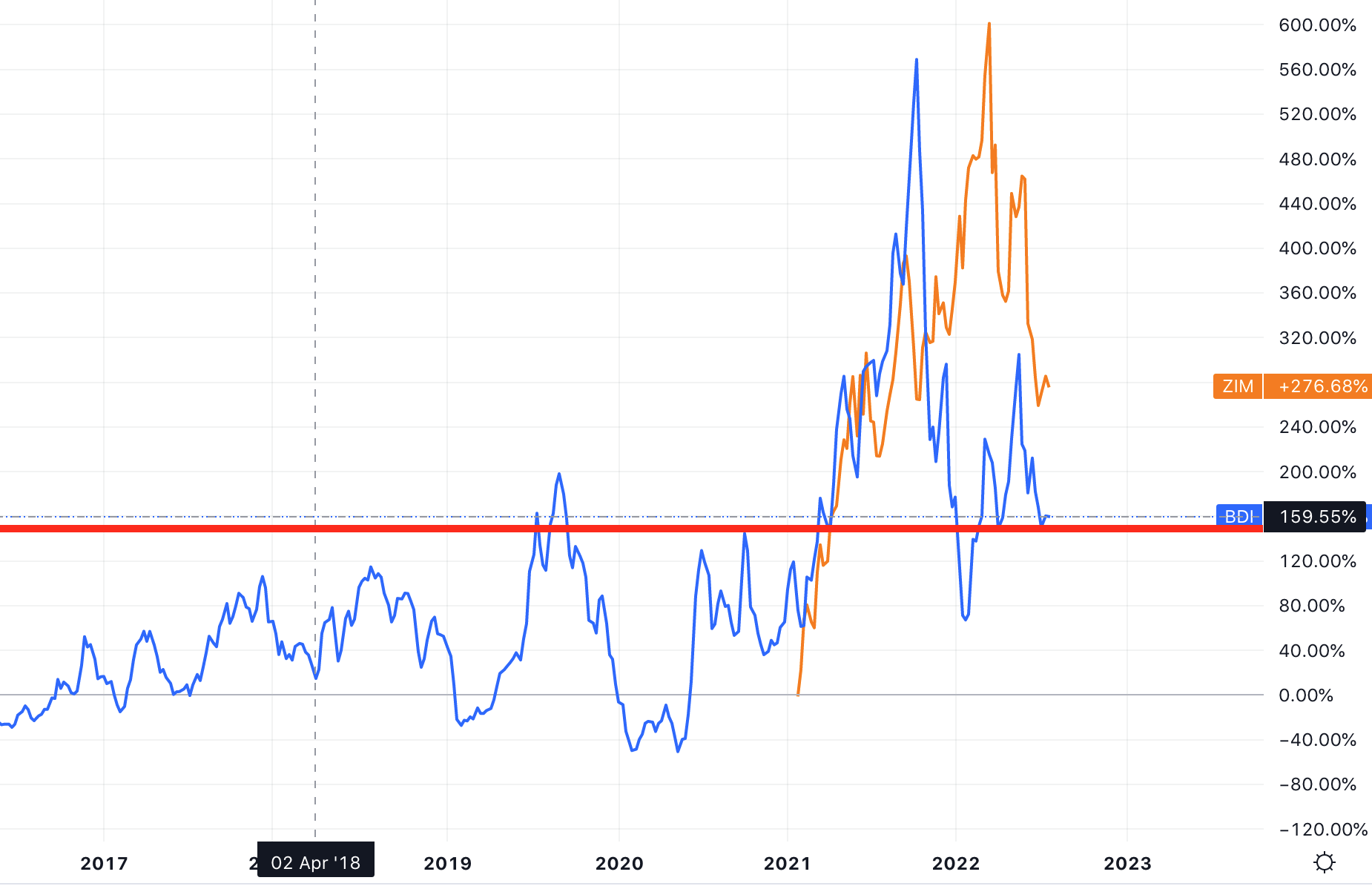

Baltic Dry Index (IMF)

I have plotted on the chart below the Baltic Dry Index (A benchmark for the price of moving the major raw materials by the ocean), indicated by the Blue line and overlaid the share price of ZIM integrated shipping (Orange line).

As you can see the pattern is remarkably similar, at the exact point when ZIM had its IPO, shipping costs and the stock price exploded in correlation. Now shipping costs have begun to normalize, due to slowing industrial demand, the stock price has also sold off by 46% from the highs. I have also noticed a large delay in the Baltic Dry Index Peak and ZIM Stock Price Peak of five to six months. As the Baltic Dry Index peaked in early October 2021 and ZIM’s stock price peaked in mid-March 2022.

ZIM and Baltic Dry Index (created by author with TradingView)

If I extrapolate this predictive delay out again for the “bottom” of the Baltic dry index which occurred at the end of January (31st) then that would mean the bottom for ZIM’s share price should be sometime in July and it does seem to have found possible support recently, but then again this could also be a “bull trap” (which I discuss in the risks section).

Note: This is an insight I have recently discovered and the historical data is fairly limited, as ZIM only IPO’d in January 2021.

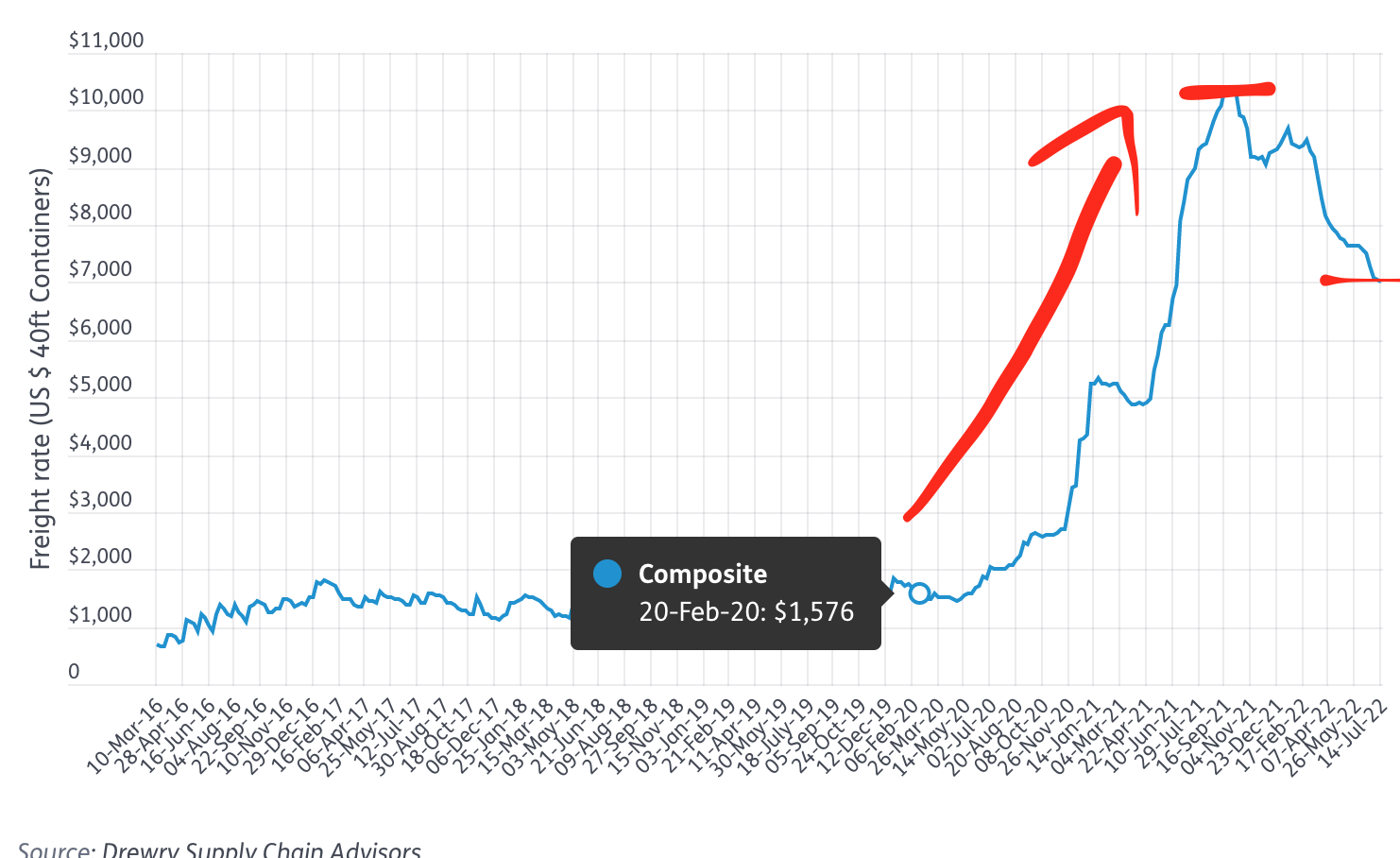

Thus, as an extra data point, the World Container Index peaked at a high of ~$10,000 at the end of September 2021. This has now slid down to ~$7,000 but is still substantially higher than pre-pandemic levels of $1,576 in February 2020. A study by McKinsey predicts that shipping rates will “Normalize” but still be “Above average levels seen in 2019”.

World Container Index (Drewry)

Given all the data points above, it looks as though ZIM is still a strong stock, especially given the ocean carries 80% of the world’s traded goods and the company is investing for future growth. In addition, the stock is trading at a low valuation relative to peers and itself historically. Let’s dive into the Business Model, Financials and Valuation for the juicy details.

Solid Business Model

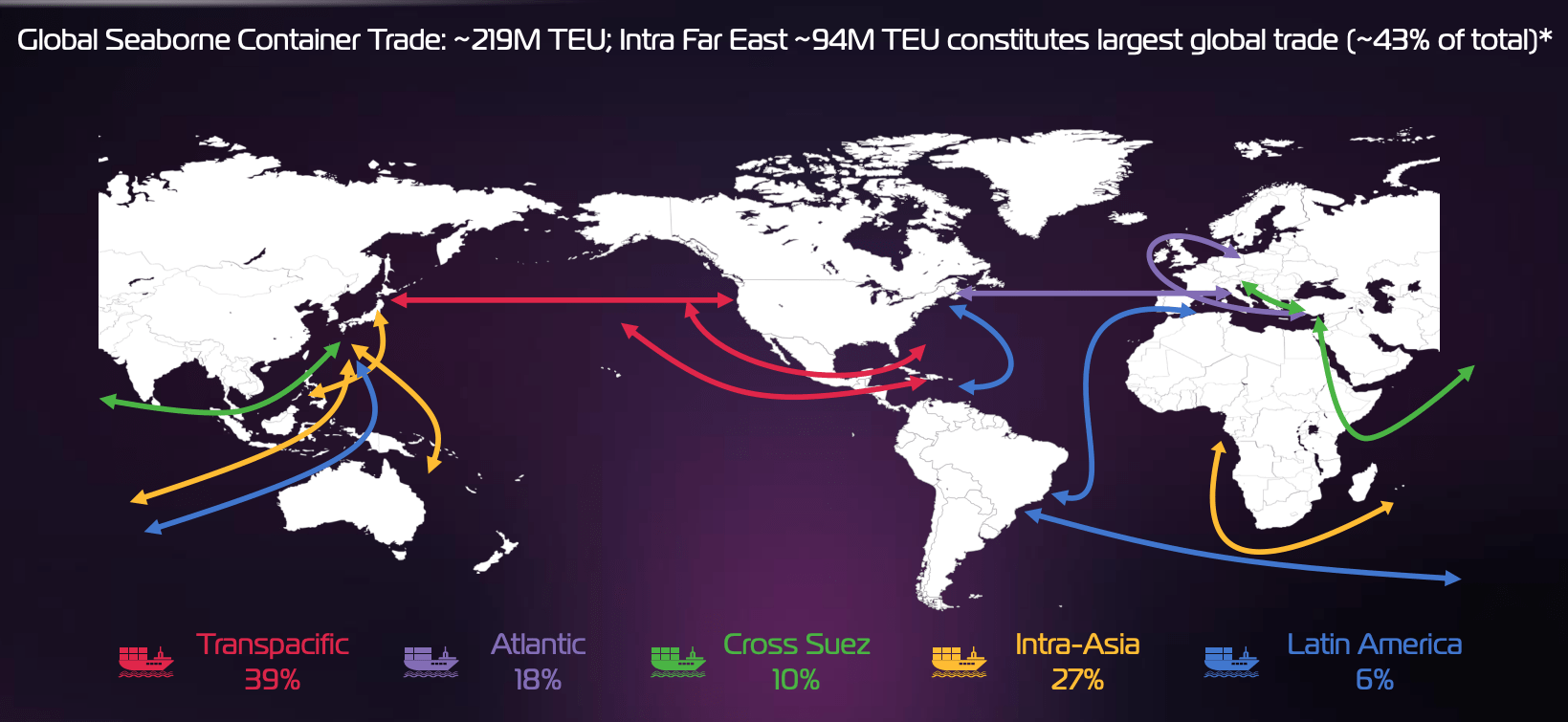

ZIM Integrated Shipping has over 4000 employees, 200 offices and ~27,000 customers. The company has strong presence across the major trade routes which include:

- Trans-Pacific – (39%)

- Intra-Asia – (27%)

- Atlantic – (18%)

- Cross Suez – (10%)

- Latin America – (6%)

Shipping ZIM Routes (Investor Presentation 2022)

ZIM has ~137 vessels but runs a flexible asset light “charted in capacity model”. In addition, management “Opportunistically” sources extra capacity in the secondhand market to complement its capacity. During the first quarter of 2022, ZIM has entered into charter agreements for 17 newbuilds, these include:

- 3 x 7,000 TEU LNG dual-fuel newbuild container vessels chartered from an affiliate of Kenon Holdings.

- 6 x 5,500 TEU wide beam newbuild vessels chartered from MPC Container Ships.

- 8 x 5,300 TEU wide beam newbuild vessels chartered from Navios Maritime Partners.

Note: TEU is a shipping industry unit which means twenty-foot equivalent unit. 20 Foot in length is the size of a traditional shipping container.

ZIM aims to be a “Global Niche Carrier” and is gradually building up shipping capacity around emerging market economies such as India, which can increase trade with Israel and Turkey. Asia-Africa as also niche routes where studies predict an increase in trade volume.

AI Investment

Despite being founded in 1945, ZIM’s management is continually innovating and reinventing themselves. The shipping industry is an antiquated industry primed for technological disruption through Blockchain and AI. At the end of June 2022, ZIM’s management took advantage of its cash flush position to provide $6 million in Venture Capital funding Data Science Consulting Group (DSG). DSG specializes in Artificial Intelligence (AI) has previously worked with ZIM on the creation of a “center of excellence” for the development of AI tools for the maritime industry. ZIM also plans to use these AI tools to improve business decisions. Now although $6 million is peanuts compared to the company’s cash flow (~$3 Billion) it does offer potential “optionality” in the stock. In addition, if ZIM is spearheading the use of technology in the industry, they could increase efficiency and capacity prediction, which would give them a competitive advantage relative to peers.

ZIM AI (Investor presentation)

ZIM Integrated’s Strong Financials

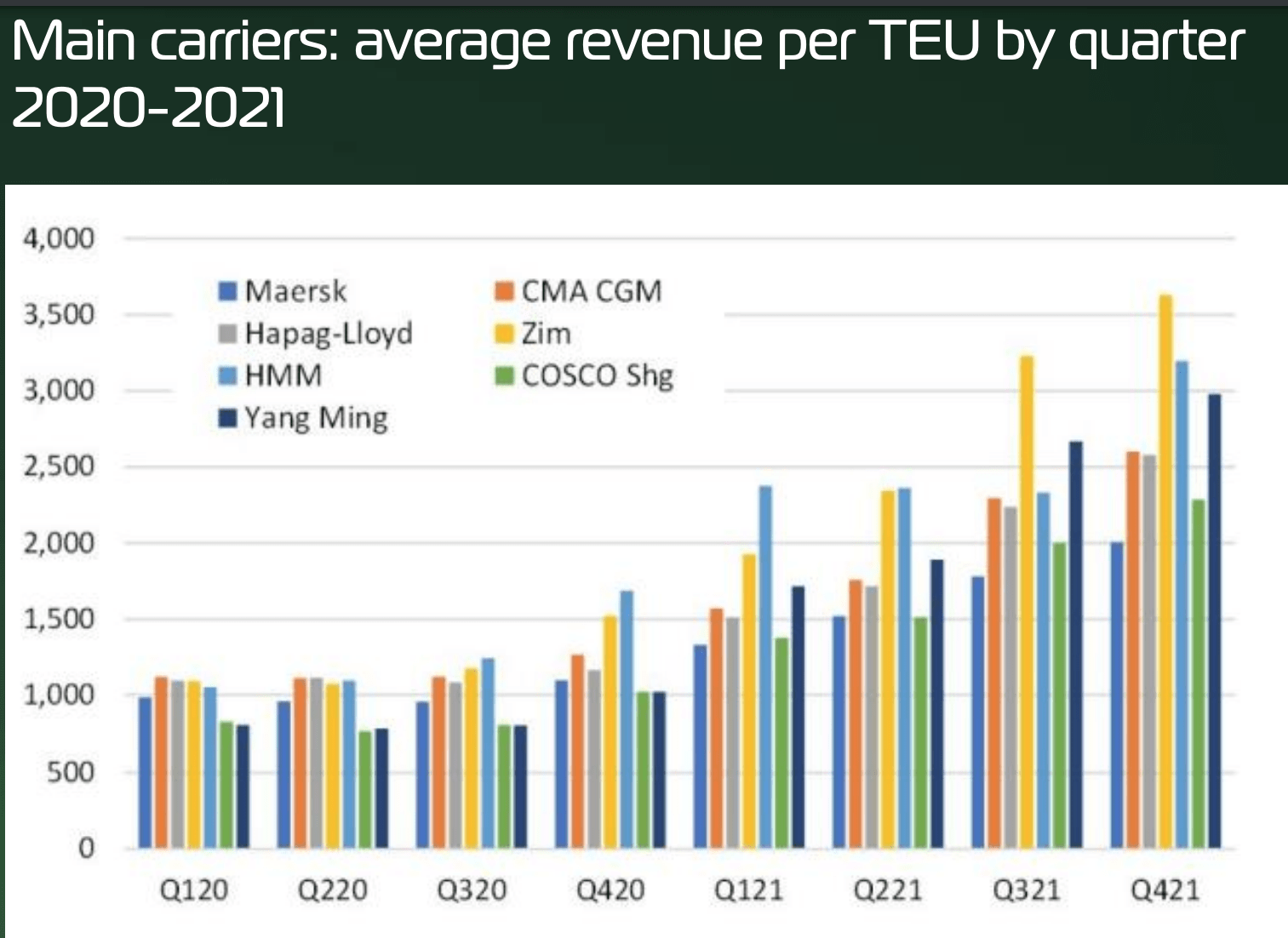

ZIM produced some tremendous financial results for the first quarter of 2022. The company generated its “highest ever” quarterly Net Income of $1.7 billion and Revenues were $3.7 billion, up a blistering 113% year over year. However, it should be noted carried volume was 859 TEU (twenty-foot equivalent units) which was only up 5% year over year. Thus, as I alluded to in the intro, the primary boost in profitability has been driven by high freight rates. The average freight rate per TEU doubled year over year to $3,484.

A comparison of the Average Revenue Per TEU for the main carriers show ZIM (yellow bar) had the highest levels of any other carrier. With over a $3,500 per TEU rate in Q421 and $3,484 in Q122 (not shown on chart). This significantly higher rate is driven by ZIM’s exposure to key East-West routes and its ability to “Opportunistically” take advantage of Spot rates.

Main Carrier comparison (investor presentation)

ZIM also generated a strong Adjusted EBITDA of $2.5 billion, up by 209% year over year. In addition, Operating Income was $2.24 billion, up by a staggering 228% year over year. While Levered Free Cash Flow increased by over 700% from $393 million in Q122, to $3.2 billion in Q22.

Despite the gloomy outlook regarding shipping prices normalizing, it was interesting to see management increase its guidance for the full year 2022. The company is forecasting Adjusted EBITDA between $7.8 and $8.2 Billion range, which would represent at least 18% growth in Adjusted EBITDA year over year.

ZIM has a fortress balance sheet with $4.8 billion in cash and short-term investments and just $171 million in long term debt.

Monster Dividend?

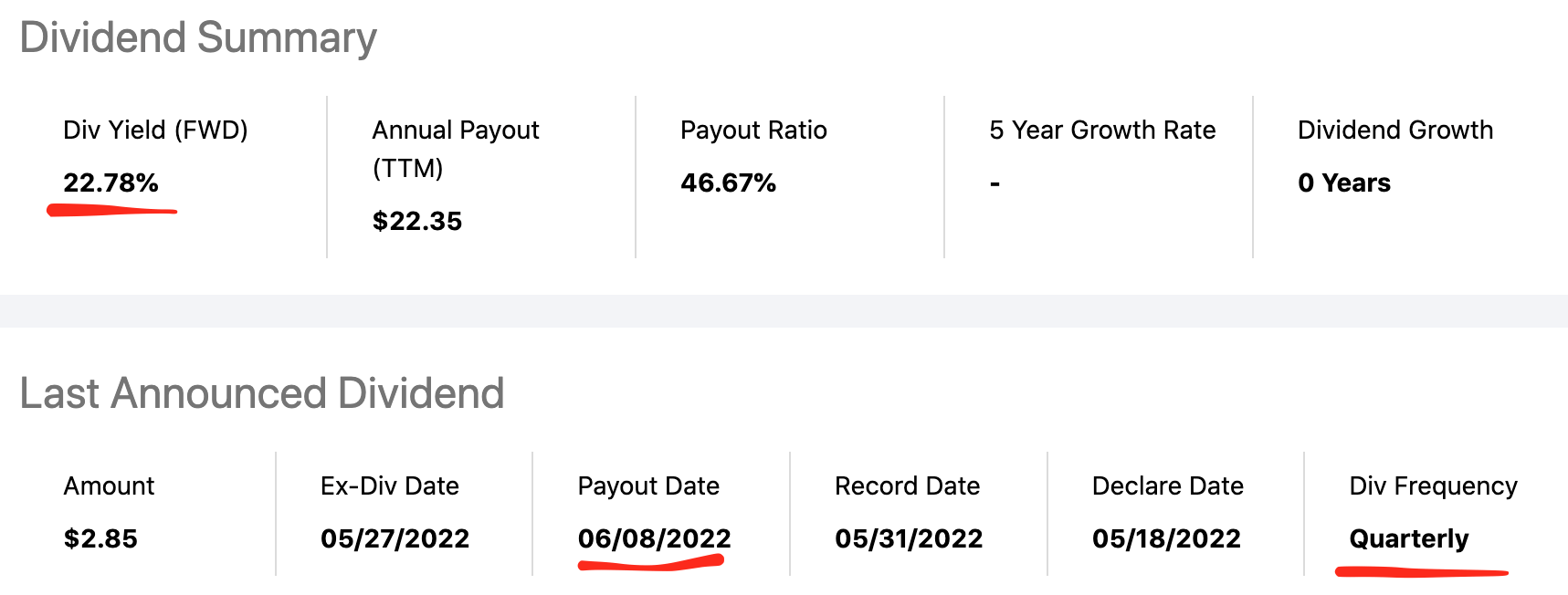

The company paid a dividend of $342 million, or $2.85 per share which represents approximately 20% of first quarter net income. ZIM’s management aims to build on this momentum and have a forward dividend yield of 22.78% which is stupendous. It should be noted this dividend is paid out quarterly and usually early in each month with the next payout being the 6th of August 2022.

ZIM Dividend (Seeking Alpha)

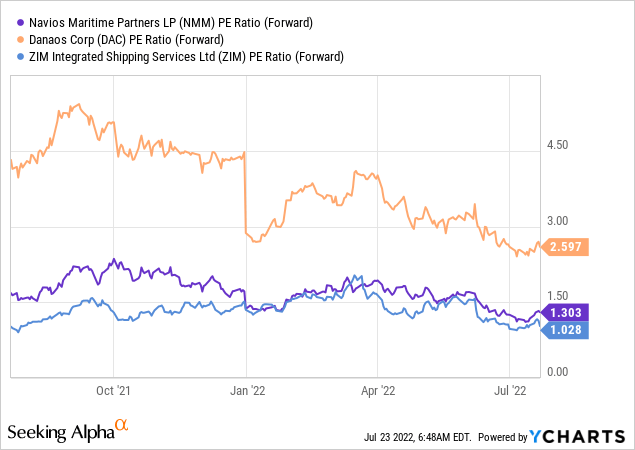

Is ZIM Stock Undervalued?

ZIM is trading at a very low forward PE ratio of just 1, which is the cheapest the stock has ever traded at historically. In addition, the stock trades at a cheaper PE ratio than industry peers such as Navios Maritime Partners L.P. (NMM) which trades at a PE (forward) Ratio = 1.3 and Danaos (DAC) which trades at a PE (forward) Ratio = 2.6, at the time of writing.

Risks

Shipping Rates Normalize/Demand Falling

In my previous post on ZIM, one of my main risks was that Shipping Rates Normalize and the stock price falls as a result, due to the relationship I mentioned at the beginning. It seems this thesis is playing out, BoA has recently slashed its price target for ZIM to $40/share on weak demand. Thus, it’s good to keep in mind that lower expectations should be set moving forward. In the words of the Legendary Investor Howard Marks, “Trees don’t grow to the sky” and the “The Market Moves in Cycles”, the shipping industry is notorious for this. In a McKinsey Study cited previously, the high shipping rates are not due to a lack of ships, but rather a lack of “effective ships” as port congestion was the main catalyst for increased rates.

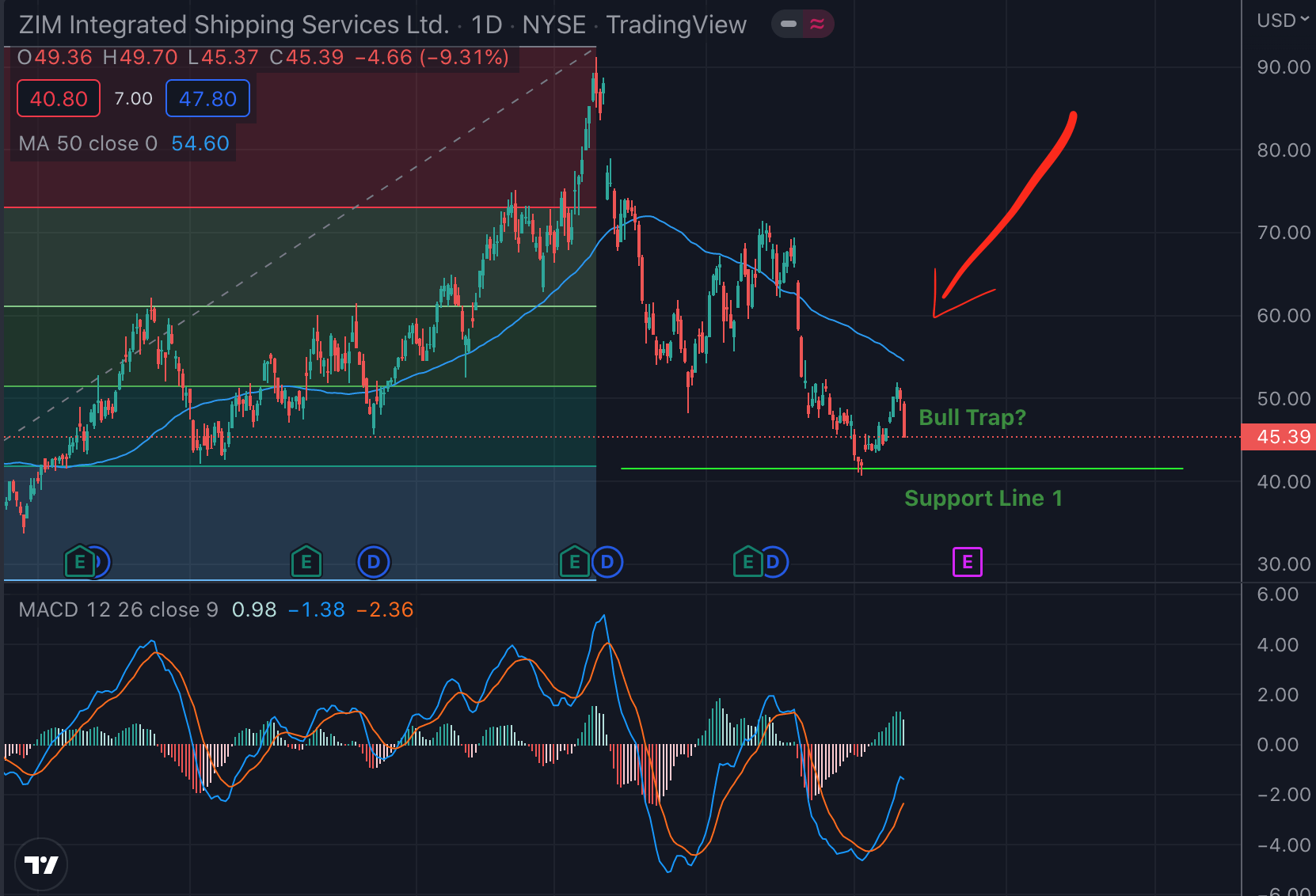

Bull Trap?

A “Bull Trap” is where a downward trend looks like it is reversing, entices “Bulls” to buy and then “Traps” them with a decline. The stock price seems to have found some support at the ~$43/share price point, thus as investors it makes sense to look for a further bounce of that support and trend reversal before entering.

Possible Bull Trap ZIM (created by author with TradingView)

Deglobalization

We have previously been through decades of “Globalization” as businesses expanded internationally to take advantage of low-cost labor and specialization in regions. However, due to complex supply chains, high potential costs and geopolitical tensions, the trend is now towards “deglobalization” in that more manufacturing is positioned locally. For instance Intel (INTC) has recently announced a new $20 Billion Ohio Factory. Although, this trend is still in the early stages, I do see signs of a world with less complex and vast supply chains moving forward.

Has the Ship Sailed?

ZIM is a tremendous company and in the short time they have been public, they have generated fantastic returns for shareholders. Management is smart, savvy and fast acting, which should help to mitigate the volatility of the shipping industry. Industrial demand is beginning to slowdown and shipping rates are starting to normalize (hence the price correction). The stock is trading at a very low valuation and the share price has hit support line but it may also be a possible “bull trap”. The mammoth dividend is enticing for investors but caution should be taken, as there is still much uncertainty. JPMorgan has recently upgraded the stock to a “HOLD” rating and that matches my forecast also.

Source link